ARR and cash flow are not the same thing. A SaaS company can grow from $500K ARR to $1M ARR while seeing almost no change in its bank balance.

The difference comes down to billing structure, revenue recognition, deferred revenue, and when customers actually pay. Understanding that difference is essential for forecasting runway, making payroll, and avoiding cash surprises.

Founders love ARR. Investors ask for it in every pitch deck. Board meetings revolve around it. Growth targets are often built around it.

Yet one of the most common founder questions is:

Why is my ARR growing but cash flat?

The answer is simple:

ARR measures recurring revenue. Cash flow measures money in the bank.

Those two numbers often move on completely different timelines.

A company can have:

- growing ARR

- strong revenue retention

- healthy customer growth

and still struggle to make payroll.

Likewise, a company can have modest ARR growth but excellent cash flow because of how customers are billed.

Understanding ARR vs cash flow and SaaS ARR vs cash flow is one of the most important concepts in SaaS finance. This guide walks through exactly why your bank balance disagrees with your ARR.

We will cover:

- why ARR does not equal cash

- annual contracts cash flow timing and subscription cash flow timing

- deferred revenue explained with SaaS examples

- monthly billing vs annual billing cash flow tradeoffs

- subscription cash flow forecasting and saas cash flow forecasting

Does ARR Equal Cash Flow?

No. ARR does not equal cash flow.

ARR is a revenue metric. Cash flow is a liquidity metric.

ARR tells you:

How much recurring revenue your business would generate annually based on current subscriptions.

Cash flow tells you:

How much money actually moved into or out of your bank account.

The distinction matters because companies spend cash, not ARR.

Payroll is paid with cash. Vendors are paid with cash. Taxes are paid with cash. Runway is measured in cash.

This is why founders who focus exclusively on ARR often find themselves surprised by cash shortages. For the broader forecasting framework, see our guide on cash flow forecasting.

What Is the Difference Between ARR and Cash?

A useful way to think about ARR vs cash:

ARR Measures Economic Value

ARR answers:

How much recurring revenue have we sold?

Cash Measures Timing

Cash answers:

When did the customer actually pay us?

These questions are related. But they are not the same. The difference becomes obvious when we look at a real contract.

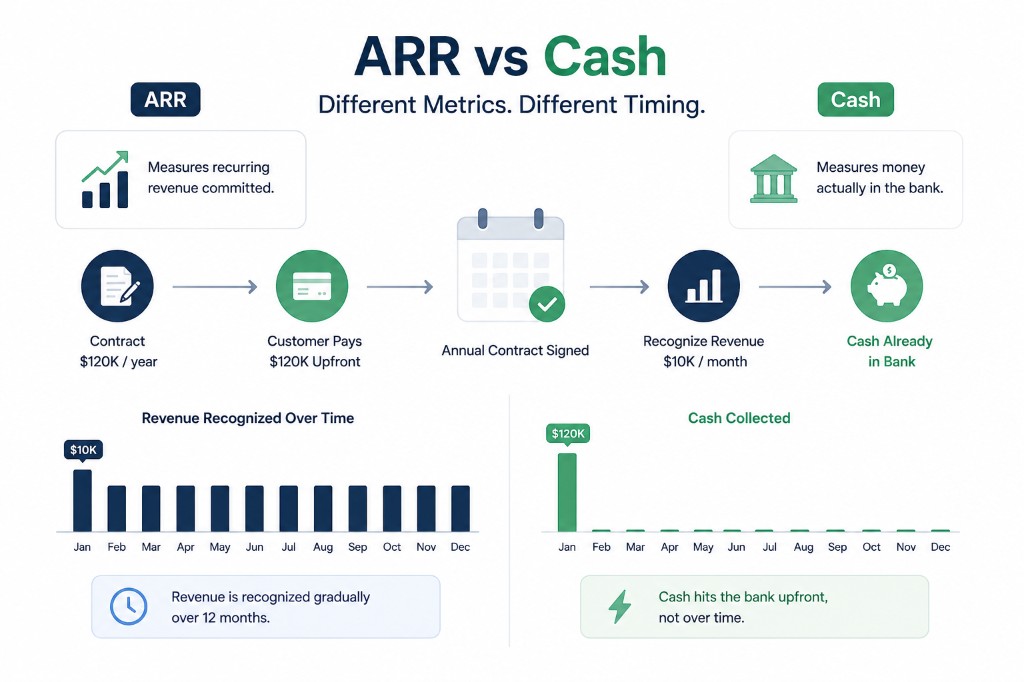

A $120,000 Annual Contract Walkthrough

Imagine you close a customer on January 1st.

Contract value:

$120,000 per year

The customer prepays the entire amount upfront.

What Happens to Cash?

On January 1st:

Bank balance +$120,000

The money immediately appears in your account. Cash flow improves instantly.

What Happens to ARR?

ARR increases by $120,000 also immediately.

What Happens to Revenue?

This is where revenue recognition vs cash diverges. Accounting rules generally require revenue to be recognized over the service period.

That means $10,000 revenue per month for the next 12 months.

Month-by-month:

| Month | Cash Received | Revenue Recognized |

|---|---|---|

| January | $120,000 | $10,000 |

| February | $0 | $10,000 |

| March | $0 | $10,000 |

| April | $0 | $10,000 |

| May | $0 | $10,000 |

| June | $0 | $10,000 |

| July | $0 | $10,000 |

| August | $0 | $10,000 |

| September | $0 | $10,000 |

| October | $0 | $10,000 |

| November | $0 | $10,000 |

| December | $0 | $10,000 |

The cash arrived once. The revenue is recognized gradually. This timing difference is the foundation of ARR vs cash flow explained and cash flow vs revenue for subscription businesses.

What Is Deferred Revenue?

The missing piece is deferred revenue.

When the customer prepays, cash increases immediately. But the company has not yet delivered 12 months of service.

The portion not yet earned becomes deferred revenue.

Deferred revenue represents:

Cash collected today for services that will be delivered later.

This is one reason SaaS founders often see healthy bank balances even when recognized revenue appears modest. The reverse can also happen: revenue may look healthy while cash remains constrained.

Understanding deferred revenue cash flow and deferred revenue examples SaaS is critical for forecasting cash flow accurately. Accounting systems like QuickBooks track deferred revenue on the balance sheet; your forecast should still model when cash actually hits the bank.

Why Is My ARR Growing but Cash Flat?

This is one of the most common questions founders ask finance teams: why is my ARR growing but cash not increasing?

Several factors can cause it.

Monthly Billing vs Annual Billing

Imagine two companies. Both have $1M ARR.

Company A bills annually. Company B bills monthly. Their ARR is identical. Their cash flow is not.

Company A (annual billing):

- customer pays $12,000 upfront

- cash enters immediately

- runway improves instantly

- deferred revenue increases

- bank balance grows

Company B (monthly billing):

- customer pays $1,000 per month

- cash arrives gradually across twelve payments

- the company receives the same amount over a year

- ARR remains identical while cash timing changes dramatically

This is the core of annual billing vs monthly billing cash flow and recurring revenue vs cash. For a rolling weekly view of when collections land, see our guide on 13-week cash flow forecasting.

Why Can Two Companies With the Same ARR Have Different Runway?

Let's compare two SaaS businesses. Both generate $1M ARR. Both have identical margins and identical expenses. The only difference is billing structure.

Company A (annual prepaid):

- cash collected upfront: $1,000,000

- immediate liquidity and longer runway

- stronger balance sheet and greater flexibility

Company B (monthly billing):

- monthly collections: roughly $83,333 per month

- same ARR, very different cash position

If revenue growth slows unexpectedly, Company B may encounter runway pressure far sooner. This is why investors often care about billing mix in addition to ARR.

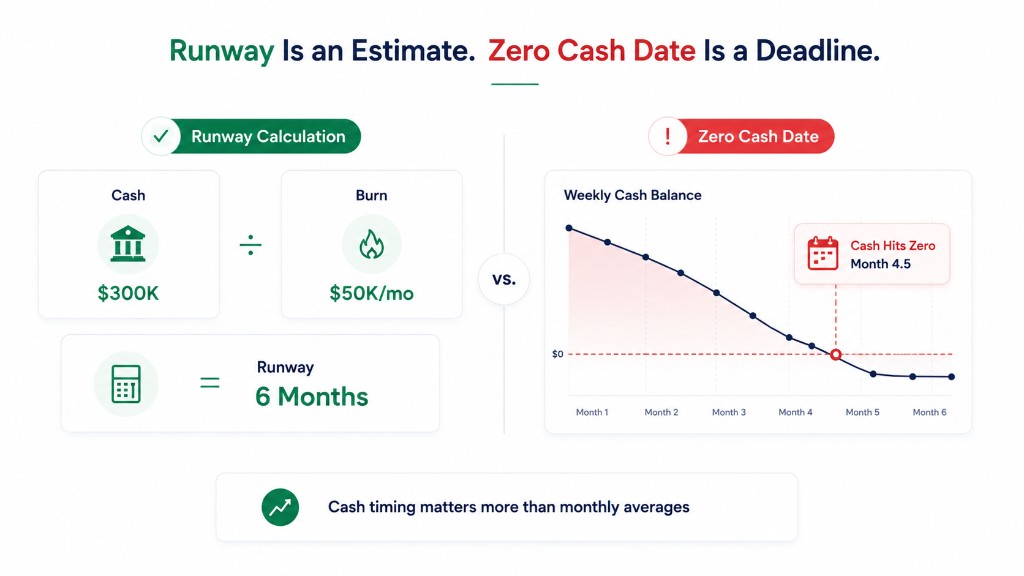

Two companies can have identical recurring revenue and completely different financial risk profiles. Model yours with the free startup runway calculator, or read our guide on runway vs burn rate for the full vocabulary.

Is Annual Billing Better Than Monthly Billing?

For cash flow, often yes. For customers, not always.

Annual contracts and annual prepaid contracts create:

- better annual billing cash flow

- more predictable collections

- longer runway

- lower churn risk

- a stronger deferred revenue position

Monthly billing creates:

- lower upfront commitment

- easier customer acquisition

- greater flexibility for buyers

There is no universal answer. But founders should understand the tradeoff. Billing structure affects cash flow more than ARR.

How Much Runway Can Annual Billing Add?

Consider a company spending $100,000 per month with net burn of $100,000 per month.

Now imagine the company converts several large customers from monthly billing to annual prepaid contracts.

The result:

- immediate cash infusion

- lower short-term liquidity risk

- more months of runway

The ARR may not change at all. The bank balance changes dramatically. This is how annual contracts affect cash flow and why annual prepaid contracts and runway are linked strategically.

Annual prepayments are often used by SaaS companies preparing for uncertain fundraising environments. For investor context on whether growth reaches profitability before cash runs out, see default alive vs default dead.

Why Revenue Recognition and Cash Collection Are Different

Founders frequently ask: why revenue does not match bank balance?

Because revenue recognition SaaS follows accounting rules. Cash collection follows customer payment behavior.

Revenue can be earned before cash is collected. Cash can be collected before revenue is earned. The two timelines rarely align perfectly.

This is why finance teams track simultaneously:

- ARR

- revenue

- deferred revenue

- cash flow

- bank balances

Each metric answers a different question.

How Should SaaS Companies Forecast Cash Flow?

This is where many companies struggle. Forecasting ARR is relatively straightforward. Forecasting cash flow requires understanding billing schedules, renewal timing, collections timing, deferred revenue, and customer payment behavior.

A company that forecasts only ARR often misses liquidity risks. SaaS cash flow forecasting and subscription revenue forecasting should answer:

- when will money arrive?

- how much cash enters the bank?

- how much runway remains?

- can payroll be covered?

These questions are ultimately more important than ARR alone. For payroll-specific timing, see Will I Make Payroll? If cash is already tight, see what happens if you miss payroll.

Why Zensus Focuses on Cash, Not Just ARR

Most dashboards stop at ARR. The problem is that founders do not make decisions using ARR. They make decisions using cash.

Questions founders actually ask include:

- will we make payroll next month?

- how much runway remains?

- what happens if renewals slip?

- what if a customer pays late?

- how does annual billing impact cash flow?

This is why Zensus models revenue, billing schedules, cash collections, deferred revenue timing, and runway projections inside a single forecast on the features page.

At Zensus, founders connect bank data via Plaid, accounting via QuickBooks, and subscription revenue via HubSpot into one financial model. See how it works for the connect-to-forecast flow.

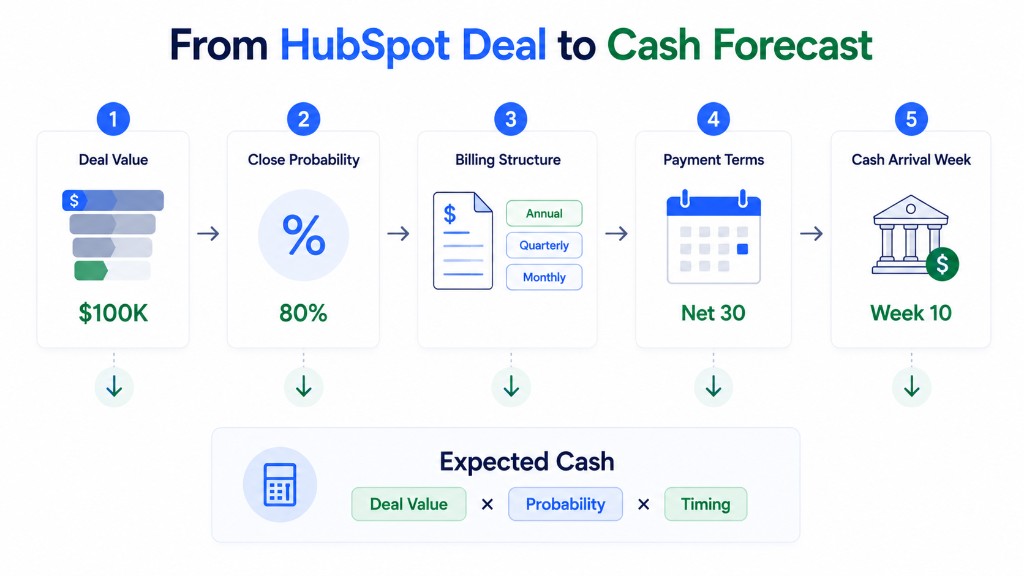

Instead of spreading annual contracts flat across twelve months, Zensus projects when cash actually hits the bank. Founders can drill from monthly to weekly to daily cash flow, run scenarios in plain English (for example, what if we lose our largest annual contract?), and get Slack alerts when a 30-day projection crosses a cash floor they set. For open pipeline deals and Commit-stage timing, see HubSpot pipeline to cash forecast.

The goal is not simply tracking ARR. The goal is understanding when cash actually hits the bank. Plans are on the pricing page.

Final Thoughts

ARR is one of the most important metrics in SaaS. But ARR is not cash.

A company can grow ARR while cash remains flat. A company can improve cash flow without increasing ARR. The difference comes down to timing.

Understanding annual contracts, deferred revenue, revenue recognition, and billing structure helps founders forecast cash more accurately and avoid unpleasant surprises.

The most successful finance teams do not ask how much ARR do we have. They ask when does the cash arrive.

Because runway, payroll, and survival depend on cash, not ARR.