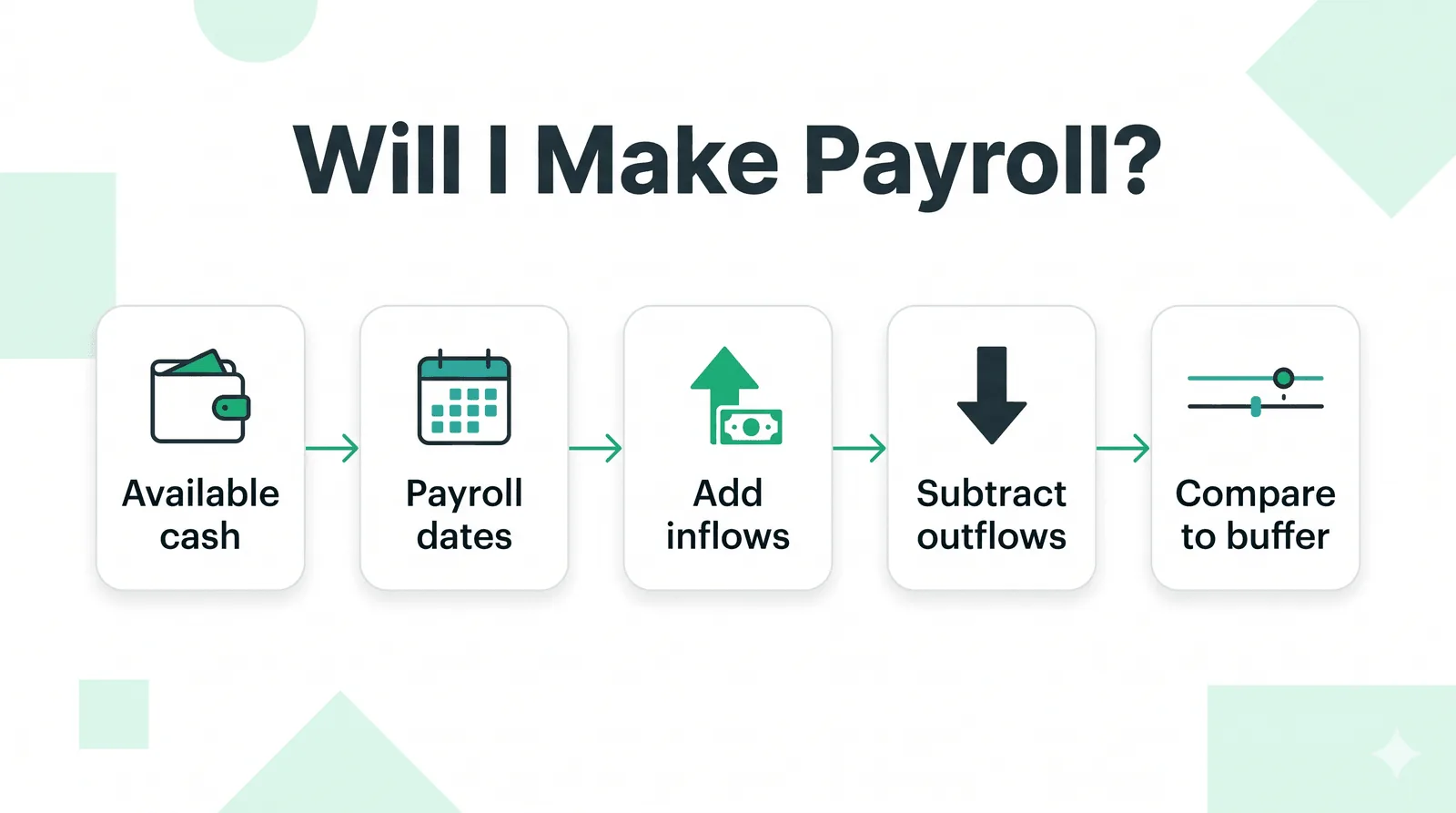

To know whether you'll make payroll, project your available cash forward to the payroll date, subtract every committed outflow due before then, add only the inflows you're confident will clear in time, and compare the result to your minimum cash buffer. If the projected balance stays above your buffer, you'll make payroll. If it dips below, you have a gap, and the whole point is to see it weeks ahead, not the morning the run is due.

Most founders answer "will I make payroll?" by glancing at their bank balance and doing some quick mental math. That feels reassuring, but the balance you see today is not the balance you'll have on payroll day. Between now and then, an annual contract might land, a big customer might pay three weeks late, rent and vendor bills clear, a tax payment goes out, and payroll itself debits your account. Whether you can cover it comes down to the timing of all those flows, and a single balance can't show you that.

This guide walks through a simple, repeatable method to answer the question with confidence, a worked example you can copy, and a checklist you can run before every payroll cycle. The method is cash flow forecasting, narrowed to the one date that matters most.

The method: project to the payroll date

The reliable way to know if you'll make payroll is to build a short cash projection that ends on your payroll date. You don't need a finance degree or a 40-tab spreadsheet. You need five inputs.

1. Start with your available cash, not your balance

Begin with the cash you can actually use today: your bank balance minus any payments that have already been authorized but haven't cleared (pending card charges, scheduled transfers, checks you've sent). This is your true starting point.

2. List every payroll date you're checking

Write down the next one to three payroll runs and their exact dates and amounts (gross pay plus employer taxes and benefits, the full amount that leaves your account, not just net pay). Use the free payroll calendar calculator to see how many pay periods fall in 2026 and 2027 and which months have three paychecks. Remember that employment tax deposits follow the IRS deposit schedule, monthly or semiweekly, so put those on their own dates too. Most shortfalls hide one cycle out, so always check at least two.

3. Add the inflows that will realistically clear in time

List the money you expect to receive before each payroll date, and be honest about timing, not hopeful:

- Invoices due, dated by when the customer actually pays, not the due date (if a client always pays net-45, use net-45)

- Subscription or recurring revenue, on the day it hits your bank; annual and quarterly contracts land in lumps, not smooth monthly slices

- Any financing, refunds, or transfers you've confirmed

Leave out anything you only hope closes. An optimistic forecast that misses is worse than no forecast.

4. Subtract every committed outflow due before then

Subtract all the cash leaving your account before each payroll date:

- The payroll run itself (the full loaded cost)

- Rent, software, and recurring vendor payments

- Loan or debt repayments

- Estimated taxes and any one-off bills you've committed to

5. Compare each payroll date to your cash buffer

For each payroll date, the projected balance is: starting cash, plus inflows that clear before the date, minus outflows due before the date. Compare that number to your minimum cash buffer, the floor you never want to drop below. If you stay above it, you'll make payroll comfortably. If you land below it, you've found a gap with enough lead time to do something about it.

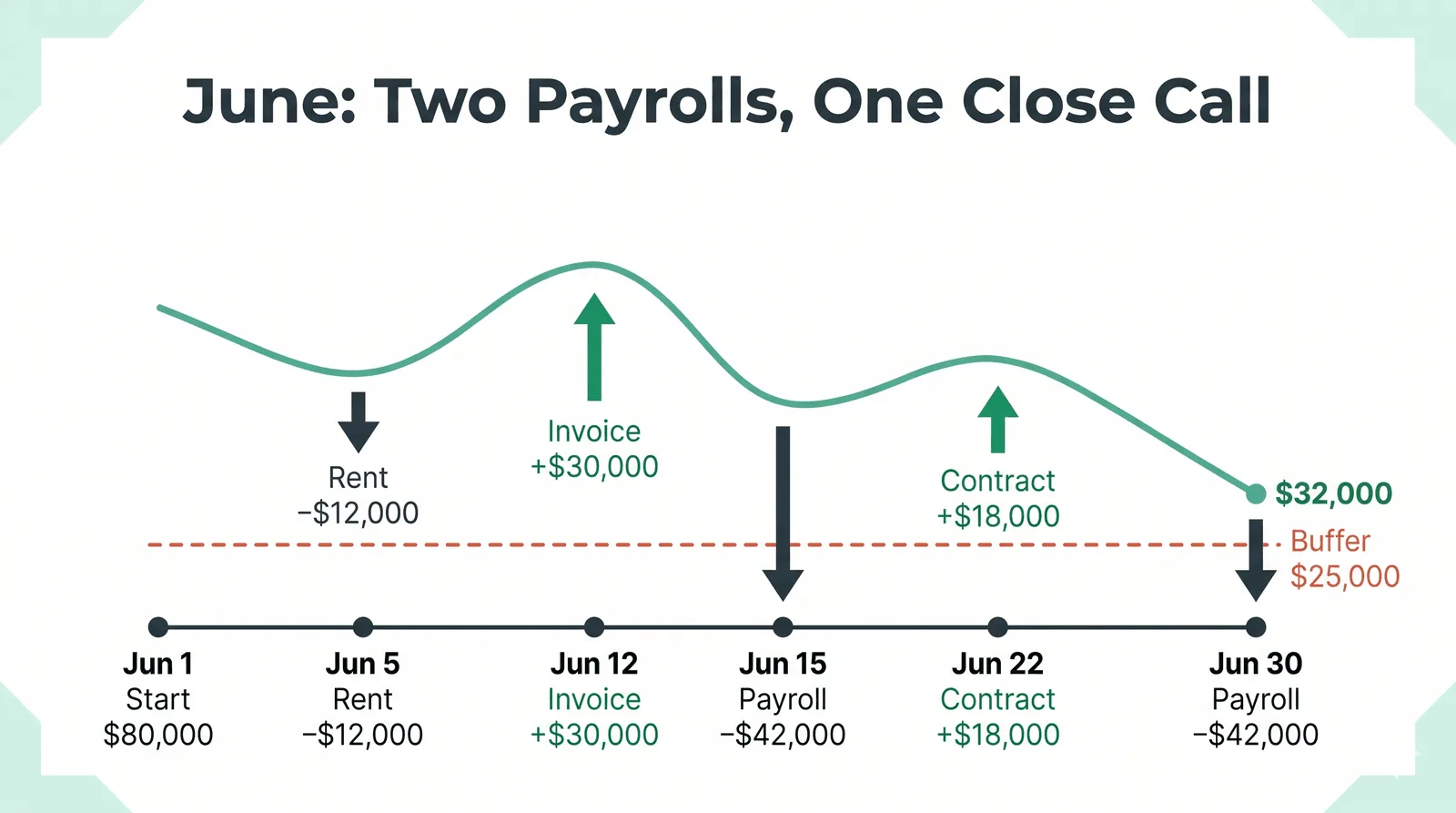

A worked example

Say it's June 1. Your numbers look like this (figures are illustrative):

- Available cash today: $80,000

- Payroll: $42,000 fully loaded, run on the 15th and the 30th

- Minimum cash buffer: $25,000

Now lay the flows on a calendar:

- June 5, rent + software clear: −$12,000

- June 12, a customer pays an overdue invoice: +$30,000

- June 15, payroll run #1: −$42,000

- June 22, quarterly contract finally lands: +$18,000

- June 30, payroll run #2: −$42,000

Walk the balance forward to each payroll date:

- Before June 15 payroll: 80,000 − 12,000 + 30,000 = $98,000, then −42,000 = $56,000. Well above the $25,000 buffer. ✅ You make this one easily.

- Before June 30 payroll: 56,000 + 18,000 = $74,000, then −42,000 = $32,000. Still above $25,000, but only by $7,000. ⚠️

The bank balance on June 1 ($80,000) looked like nearly two payrolls of cushion. The projection tells the real story: the second run lands you within $7,000 of your floor, and that's only if the quarterly contract clears on the 22nd as expected. If it slips to July, June 30 payroll drops you to $14,000, below your buffer. You now know, on June 1, exactly which inflow to chase and by when.

That gap is invisible on a bank statement and invisible in a flat "monthly revenue minus monthly expenses" model. It only shows up when you place each flow on the date it actually moves.

The mistake most founders make

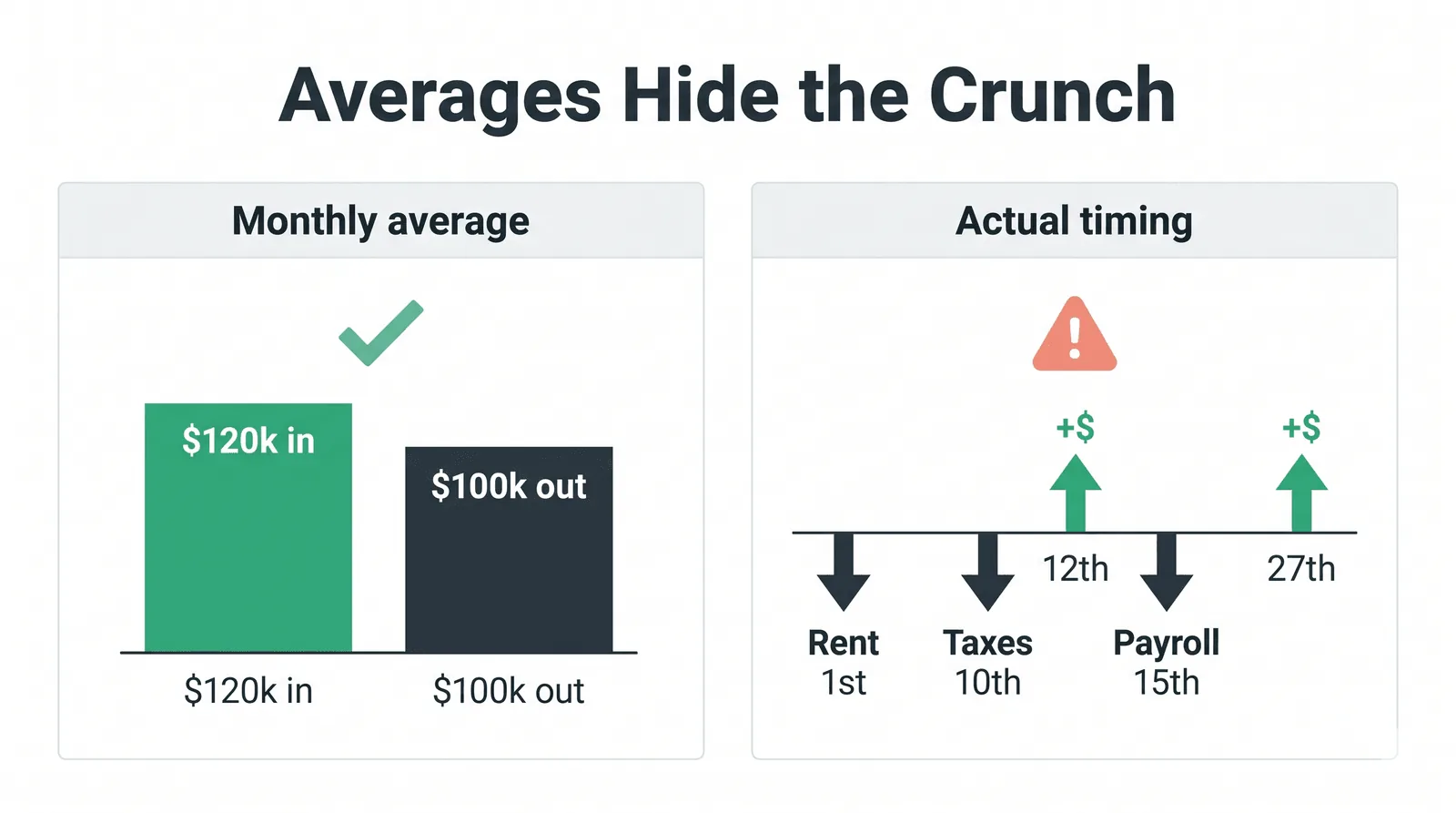

The single most common payroll-cash error is using averages instead of timing. "We bring in about $120k a month and spend about $100k, so we're fine" hides the fact that the $120k arrives in two lumps on the 12th and 27th while payroll, rent, and a tax bill all clear before the 15th. Monthly averages smooth over exactly the timing mismatches that cause a missed payroll.

The second mistake is optimistic receivables: assuming customers pay on the due date. Date your inflows by when each customer actually pays, and your forecast stops lying to you.

How far ahead should you forecast payroll?

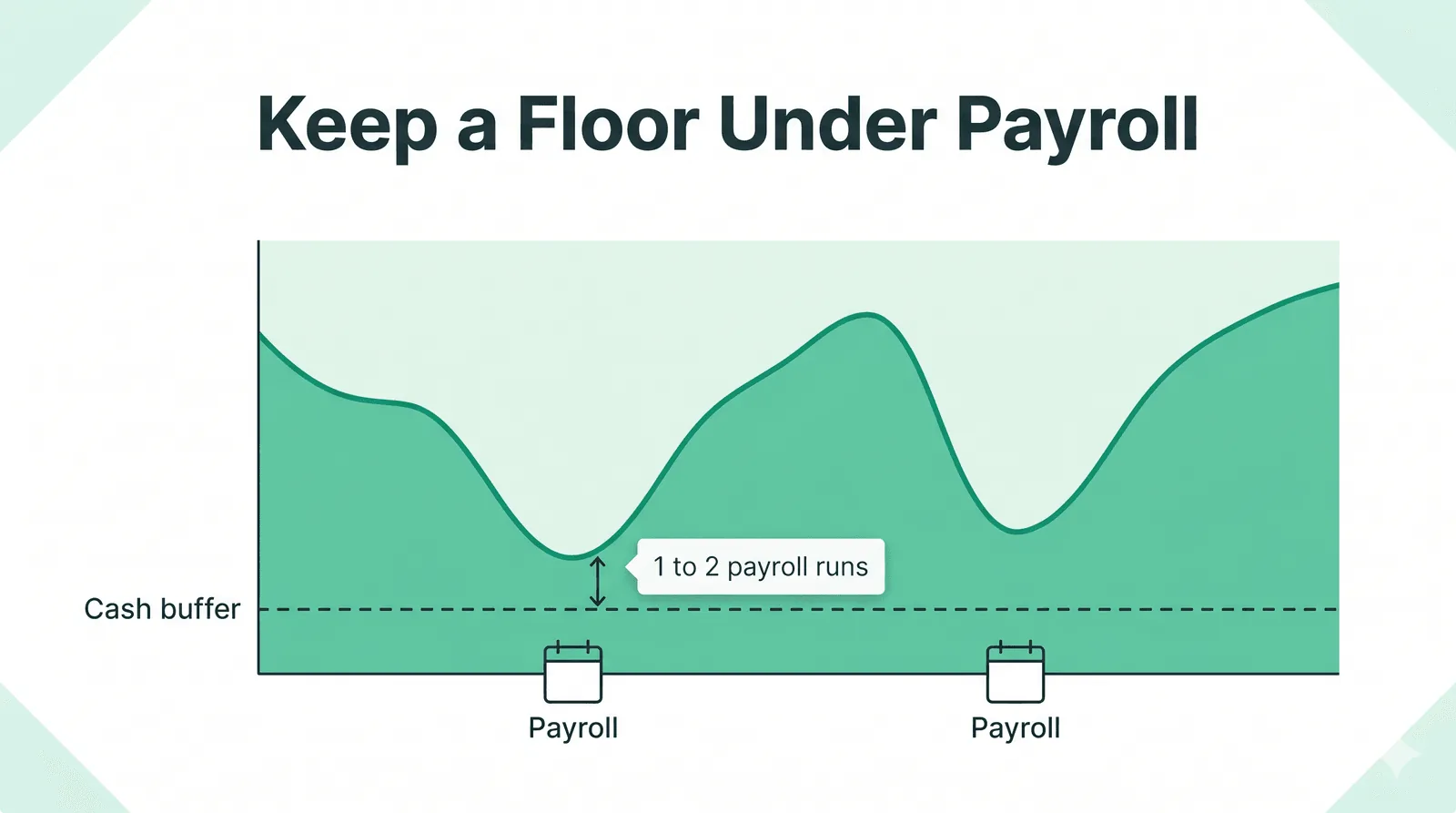

At least two full payroll cycles, roughly 30 to 60 days for most businesses. One cycle isn't enough: if you only look at the next run, you can clear it and still be walking into a wall on the one after. Two cycles gives you the lead time to collect a receivable, delay a discretionary payment, draw on a line of credit, or trim spend, all of which take days or weeks, not hours. If you want a longer horizon, a 13-week cash flow forecast extends the same discipline a full quarter out.

What's a safe cash buffer before payroll?

Keep at least one full payroll run in reserve above your projected low point, and ideally two. As a broader floor, many founders target two to six months of total operating expenses. The lumpier and less predictable your revenue, the larger that buffer should be: a business living on a few large annual contracts needs more cushion than one with smooth monthly subscriptions, because a single late payment moves the needle further. For context on how thin most buffers run: JPMorgan Chase Institute's analysis of nearly 600,000 small businesses found the median holds just 27 cash buffer days, under a month of typical outflows.

Your "will I make payroll" checklist

Run this before every payroll cycle:

- Start from available cash (balance minus pending payments)

- Map the next two payroll dates and their fully loaded amounts

- Add only inflows you're confident clear in time, dated by actual payment behavior

- Subtract every committed outflow due before each payroll date

- Check the projected balance on each date against your minimum buffer

- If any date lands below the buffer, identify the specific inflow to chase or outflow to defer now, while you have time

- Re-run it whenever a big invoice, contract, or expense changes

How Zensus answers this automatically

Doing this by hand works, right up until your forecast goes stale the moment a transaction clears or an invoice slips. That's the part Zensus automates.

Connect your bank (via Plaid), QuickBooks, and HubSpot, and Zensus places every recurring inflow and outflow (each payroll run, your annual and quarterly contracts, and your committed bills) on the exact day it actually hits your account. Your cash flow forecast updates in real time as transactions clear, so the balance projected to each payroll date is always current, not a snapshot from last week. How Zensus handles your financial data is documented on the security page.

Then set your cash floor once. Zensus watches your rolling 30-day projection and fires a Slack alert the moment it's on track to cross that floor, and re-alerts if the breach moves earlier or your minimum balance drops further. Instead of asking "will I make payroll?" every Monday, you find out the instant the answer changes.

If you'd rather see it than build it, you can start a 14-day free trial (plans are on the pricing page) and have your live cash flow forecast and your next two payroll dates in front of you in a couple of minutes.